Monetary policy of the United States

| This article is part of a series on |

| Banking in the United States of America |

|---|

|

|

Lending |

|

United States portal |

Monetary policy concerns the actions of a central bank or other regulatory authorities that determine the size and rate of growth of the money supply.

In the United States, the Federal Reserve is in charge of monetary policy, and implements it primarily by performing operations that influence short-term interest rates.

Money supply

The money supply has different components, generally broken down into "narrow" and "broad" money, reflecting the different degrees of liquidity ('spendability') of each different type, as broader forms of money can be converted into narrow forms of money (or may be readily accepted as money by others, such as personal checks).[1]

For example, demand deposits are technically promises to pay on demand, while savings deposits are promises to pay subject to some withdrawal restrictions, and Certificates of Deposit are promises to pay only at certain specified dates; each can be converted into money, but "narrow" forms of money can be converted more readily. The Federal Reserve directly controls only the most narrow form of money, physical cash outstanding along with the reserves of banks throughout the country (known as M0 or the monetary base); the Federal Reserve indirectly influences the supply of other types of money.[1]

Broad money includes money held in deposit balances in banks and other forms created in the financial system. Basic economics also teaches that the money supply shrinks when loans are repaid;[2][3] however, the money supply will not necessarily decrease depending on the creation of new loans and other effects. Other than loans, investment activities of commercial banks and the Federal Reserve also increase and decrease the money supply.[4] Discussion of "money" often confuses the different measures and may lead to misguided commentary on monetary policy and misunderstandings of policy discussions.[5]

Structure of modern US institutions

Federal Reserve

Monetary policy in the US is determined and implemented by the US Federal Reserve System, commonly referred to as the Federal Reserve. Established in 1913 by the Federal Reserve Act to provide central banking functions,[6] the Federal Reserve System is a quasi-public institution. Ostensibly, the Federal Reserve Banks are 12 private banking corporations;[7][8][9] they are independent in their day-to-day operations, but legislatively accountable to Congress through the auspices of Federal Reserve Board of Governors.

The Board of Governors is an independent governmental agency consisting of seven officials and their support staff of over 1800 employees headquartered in Washington, D.C.[10] It is independent in the sense that the Board currently operates without official obligation to accept the requests or advice of any elected official with regard to actions on the money supply,[11] and its methods of funding also preserve independence. The Governors are nominated by the President of the United States, and nominations must be confirmed by the U.S. Senate.[12]

The presidents of the Federal Reserve Banks are nominated by each bank's respective Board of Directors, but must also be approved by the Board of Governors of the Federal Reserve. The Chairman of the Federal Reserve Board is generally considered to have the most important position, followed by the president of the Federal Reserve Bank of New York.[12] The Federal Reserve System is primarily funded by interest collected on their portfolio of securities from the US Treasury, and the Fed has broad discretion in drafting its own budget,[13] but, historically, nearly all the interest the Federal Reserve collects is rebated to the government each year.[14]

The Federal Reserve has three main mechanisms for manipulating the money supply. It can buy or sell treasury securities. Selling securities has the effect of reducing the monetary base (because it accepts money in return for purchase of securities), taking that money out of circulation. Purchasing treasury securities increases the monetary base (because it pays out hard currency in exchange for accepting securities). Secondly, the discount rate can be changed. And finally, the Federal Reserve can adjust the reserve requirement, which can affect the money multiplier; the reserve requirement is adjusted only infrequently, and was last adjusted in 1992.[15]

In practice, the Federal Reserve uses open market operations to influence short-term interest rates, which is the primary tool of monetary policy. The federal funds rate, for which the Federal Open Market Committee announces a target on a regular basis, reflects one of the key rates for interbank lending. Open market operations change the supply of reserve balances, and the federal funds rate is sensitive to these operations.[16]

In theory, the Federal Reserve has unlimited capacity to influence this rate, and although the federal funds rate is set by banks borrowing and lending funds to each other, the federal funds rate generally stays within a limited range above and below the target (as participants are aware of the Fed's power to influence this rate).

Assuming a closed economy, where foreign capital or trade does not affect the money supply, when money supply increases, interest rates go down. Businesses and consumers have a lower cost of capital and can increase spending and capital improvement projects. This encourages short-term growth. Conversely, when the money supply falls, interest rates go up, increasing the cost of capital and leading to more conservative spending and investment. The Federal reserve increases interest rates to combat Inflation.

Private commercial banks

When money is deposited in a bank, it can then be lent out to another person. If the initial deposit was $100 and the bank lends out $100 to another customer the money supply has increased by $100. However, because the depositor can ask for the money back, banks have to maintain minimum reserves to service customer needs. If the reserve requirement is 10% then, in the earlier example, the bank can lend $90 and thus the money supply increases by only $90. The reserve requirement therefore acts as a limit on this multiplier effect. Because the reserve requirement only applies to the more narrow forms of money creation (corresponding to M1), but does not apply to certain types of deposits (such as time deposits), reserve requirements play a limited role in monetary policy.[17]

Money creation

Currently, the US government maintains over US$800 billion in cash money (primarily Federal Reserve Notes) in circulation throughout the world,[18][19] up from a sum of less than $30 billion in 1959. Below is an outline of the process which is currently used to control the amount of money in the economy. The amount of money in circulation generally increases to accommodate money demanded by the growth of the country's production. The process of money creation usually goes as follows:

- Banks go through their daily transactions. Of the total money deposited at banks, significant and predictable proportions often remain deposited, and may be referred to as "core deposits." Banks use the bulk of "non-moving" money (their stable or "core" deposit base) by loaning it out.[20] Banks have a legal obligation to keep a certain fraction of bank deposit money on-hand at all times.[21]

- In order to raise additional money to cover excess spending, Congress increases the size of the National Debt by issuing securities typically in the form of a Treasury Bond[22] (see Treasury security). It offers the Treasury security for sale, and someone pays cash to the government in exchange. Banks are often the purchasers of these securities, and these securities currently play a crucial role in the process.

- The 12-person Federal Open Market Committee, which consists of the heads of the Federal Reserve System (the seven Federal governors and five bank presidents), meets eight times a year to determine how they would like to influence the economy.[23] They create a plan called the country's "monetary policy" which sets targets for things such as interest rates.[24]

- Every business day, the Federal Reserve System engages in Open market operations.[25] If the Federal Reserve wants to increase the money supply, it will buy securities (such as U.S. Treasury Bonds) anonymously from banks in exchange for dollars. If the Federal Reserve wants to decrease the money supply, it will sell securities to the banks in exchange for dollars, taking those dollars out of circulation.[26][27] When the Federal Reserve makes a purchase, it credits the seller's reserve account (with the Federal Reserve). The money that it deposits into the seller's account is not transferred from any existing funds, therefore it is at this point that the Federal Reserve has created High-powered money.

- By means of open market operations, the Federal Reserve affects the free reserves of commercial banks in the country.[28] Anna Schwartz explains that "if the Federal Reserve increases reserves, a single bank can make loans up to the amount of its excess reserves, creating an equal amount of deposits".[26][27][29]

- Since banks have more free reserves, they may loan out the money, because holding the money would amount to accepting the cost of foregone interest[28][30] When a loan is granted, a person is generally granted the money by adding to the balance on their bank account.[31]

- This is how the Federal Reserve's high-powered money is multiplied into a larger amount of broad money, through bank loans; as written in a particular case study, "as banks increase or decrease loans, the nation's (broad) money supply increases or decreases."[3] Once granted these additional funds, the recipient has the option to withdraw physical currency (dollar bills and coins) from the bank, which will reduce the amount of money available for further on-lending (and money creation) in the banking system.[32]

- In many cases, account-holders will request cash withdrawals, so banks must keep a supply of cash handy. When they believe they need more cash than they have on hand, banks can make requests for cash with the Federal Reserve. In turn, the Federal Reserve examines these requests and places an order for printed money with the US Treasury Department.[33] The Treasury Department sends these requests to the Bureau of Engraving and Printing (to make dollar bills) and the Bureau of the Mint (to stamp the coins).

- The U.S. Treasury sells this newly printed money to the Federal Reserve for the cost of printing. This is about 6 cents per bill for any denomination.[34] Aside from printing costs, the Federal Reserve must pledge collateral (typically government securities such as Treasury bonds) to put new money, which does not replace old notes, into circulation.[35] This printed cash can then be distributed to banks, as needed.

Though the Federal Reserve authorizes and distributes the currency printed by the Treasury (the primary component of the narrow monetary base), the broad money supply is primarily created by commercial banks through the money multiplier mechanism.[29][31][36][37] One textbook summarizes the process as follows:

"The Fed" controls the money supply in the United States by controlling the amount of loans made by commercial banks. New loans are usually in the form of increased checking account balances, and since checkable deposits are part of the money supply, the money supply increases when new loans are made ...[38]

This type of money is convertible into cash when depositors request cash withdrawals, which will require banks to limit or reduce their lending.[39][32] The vast majority of the broad money supply throughout the world represents current outstanding loans of banks to various debtors.[38][40][41] A very small amount of U.S. currency still exists as "United States Notes", which have no meaningful economic difference from Federal Reserve notes in their usage, although they departed significantly in their method of issuance into circulation. The currency distributed by the Federal Reserve has been given the official designation of "Federal Reserve Notes."[42]

Significant effects

In 2005, the Federal Reserve held approximately 9% of the national debt[43] as assets against the liability of printed money. In previous periods, the Federal Reserve has used other debt instruments, such as debt securities issued by private corporations. During periods when the national debt of the United States has declined significantly (such as happened in fiscal years 1999 and 2000), monetary policy and financial markets experts have studied the practical implications of having "too little" government debt: both the Federal Reserve and financial markets use the price information, yield curve and the so-called risk free rate extensively.[44]

Experts are hopeful that other assets could take the place of National Debt as the base asset to back Federal Reserve notes, and Alan Greenspan, long the head of the Federal Reserve, has been quoted as saying, "I am confident that U.S. financial markets, which are the most innovative and efficient in the world, can readily adapt to a paydown of Treasury debt by creating private alternatives with many of the attributes that market participants value in Treasury securities."[45] In principle, the government could still issue debt securities in significant quantities while having no net debt, and significant quantities of government debt securities are also held by other government agencies.

Although the U.S. government receives income overall from seigniorage, there are costs associated with maintaining the money supply.[41][46] Leading ecological economist and steady-state theorist Herman Daly, claims that "over 95% of our [broad] money supply [in the United States] is created by the private banking system (demand deposits) and bears interest as a condition of its existence,"[41] a conclusion drawn from the Federal Reserve's ultimate dependence on increased activity in fractional reserve lending when it exercises open market operations.[47] Economist Eric Miller criticizes Daly's logic because money is created in the banking system in response to demand for the money,[48] which justifies cost.

Thus, use of expansionary open market operations typically generates more debt in the private sector of society (in the form of additional bank deposits).[49] The private banking system charges interest to borrowers as a cost to borrow the money.[3][31][50] The interest costs are borne by those that have borrowed,[3][31] and without this borrowing, open market operations would be unsuccessful in maintaining the broad money supply,[30] though alternative implementations of monetary policy could be used. Depositors of funds in the banking system are paid interest on their savings (or provided other services, such as checking account privileges or physical security for their "cash"), as compensation for "lending" their funds to the bank.

Increases (or contractions) of the money supply corresponds to growth (or contraction) in interest-bearing debt in the country.[3][30][41] The concepts involved in monetary policy may be widely misunderstood in the general public, as evidenced by the volume of literature on topics such as "Federal Reserve conspiracy" and "Federal Reserve fraud."[51]

Uncertainties

A few of the uncertainties involved in monetary policy decision making are described by the federal reserve:[52]

- While these policy choices seem reasonably straightforward, monetary policy makers routinely face certain notable uncertainties. First, the actual position of the economy and growth in aggregate demand at any time are only partially known, as key information on spending, production, and prices becomes available only with a lag. Therefore, policy makers must rely on estimates of these economic variables when assessing the appropriate course of policy, aware that they could act on the basis of misleading information. Second, exactly how a given adjustment in the federal funds rate will affect growth in aggregate demand—in terms of both the overall magnitude and the timing of its impact—is never certain. Economic models can provide rules of thumb for how the economy will respond, but these rules of thumb are subject to statistical error. Third, the growth in aggregate supply, often called the growth in potential output, cannot be measured with certainty.

- In practice, as previously noted, monetary policy makers do not have up-to-the-minute information on the state of the economy and prices. Useful information is limited not only by lags in the collection and availability of key data but also by later revisions, which can alter the picture considerably. Therefore, although monetary policy makers will eventually be able to offset the effects that adverse demand shocks have on the economy, it will be some time before the shock is fully recognized and—given the lag between a policy action and the effect of the action on aggregate demand—an even longer time before it is countered. Add to this the uncertainty about how the economy will respond to an easing or tightening of policy of a given magnitude, and it is not hard to see how the economy and prices can depart from a desired path for a period of time.

- The statutory goals of maximum employment and stable prices are easier to achieve if the public understands those goals and believes that the Federal Reserve will take effective measures to achieve them.

- Although the goals of monetary policy are clearly spelled out in law, the means to achieve those goals are not. Changes in the FOMC's target federal funds rate take some time to affect the economy and prices, and it is often far from obvious whether a selected level of the federal funds rate will achieve those goals.

Opinions of the Federal Reserve

The Federal Reserve is lauded by some economists, while being the target of scathing criticism by other economists, legislators, and sometimes members of the general public. The former Chairman of the Federal Reserve Board, Ben Bernanke, is one of the leading academic critics of the Federal Reserve's policies during the Great Depression.[53]

Achievements

One of the functions of a central bank is to facilitate the transfer of funds through the economy, and the Federal Reserve System is largely responsible for the efficiency in the banking sector. There have also been specific instances which put the Federal Reserve in the spotlight of public attention. For instance, after the stock market crash in 1987, the actions of the Fed are generally believed to have aided in recovery. Also, the Federal Reserve is credited for easing tensions in the business sector with the reassurances given following the 9/11 terrorist attacks on the United States.[54]

Criticisms

The Federal Reserve has been the target of various criticisms, involving: accountability, effectiveness, opacity, inadequate banking regulation, and potential market distortion. Federal Reserve policy has also been criticized for directly and indirectly benefiting large banks instead of consumers. For example, regarding the Federal Reserve's response to the 2007–2010 financial crisis, Nobel laureate Joseph Stiglitz explained how the U.S. Federal Reserve was implementing another monetary policy —creating currency— as a method to combat the liquidity trap.[55]

By creating $600 billion and inserting this directly into banks the Federal Reserve intended to spur banks to finance more domestic loans and refinance mortgages. However, banks instead were spending the money in more profitable areas by investing internationally in emerging markets. Banks were also investing in foreign currencies which Stiglitz and others point out may lead to currency wars while China redirects its currency holdings away from the United States.[56]

Auditing

The Federal Reserve is subject to different requirements for transparency and audits than other government agencies, which its supporters claim is another element of the Fed's independence. Although the Federal Reserve has been required by law to publish independently audited financial statements since 1999, the Federal Reserve is not audited in the same way as other government agencies. Some confusion can arise because there are many types of audits, including: investigative or fraud audits; and financial audits, which are audits of accounting statements; there are also compliance, operational, and information system audits.

The Federal Reserve's annual financial statements are audited by an outside auditor. Similar to other government agencies, the Federal Reserve maintains an Office of the Inspector General, whose mandate includes conducting and supervising "independent and objective audits, investigations, inspections, evaluations, and other reviews of Board programs and operations."[57] The Inspector General's audits and reviews are available on the Federal Reserve's website.[58][59]

The Government Accountability Office (GAO) has the power to conduct audits, subject to certain areas of operations that are excluded from GAO audits; other areas may be audited at specific Congressional request, and have included bank supervision, government securities activities, and payment system activities.[60][61] The GAO is specifically restricted any authority over monetary policy transactions;[60] the New York Times reported in 1989 that "such transactions are now shielded from outside audit, although the Fed influences interest rates through the purchase of hundreds of billions of dollars in Treasury securities."[62] As mentioned above, it was in 1999 that the law governing the Federal Reserve was amended to formalize the already-existing annual practice of ordering independent audits of financial statements for the Federal Reserve Banks and the Board;[63] the GAO's restrictions on auditing monetary policy continued, however.[61]

Congressional oversight on monetary policy operations, foreign transactions, and the FOMC operations is exercised through the requirement for reports and through semi-annual monetary policy hearings.[61] Scholars have conceded that the hearings did not prove an effective means of increasing oversight of the Federal Reserve, perhaps because "Congresspersons prefer to bash an autonomous and secretive Fed for economic misfortune rather than to share the responsibility for that misfortune with a fully accountable Central Bank," although the Federal Reserve has also consistently lobbied to maintain its independence and freedom of operation.[64]

Fulfillment of wider economic goals

By law, the goals of the Fed's monetary policy are: high employment, sustainable growth, and stable prices.[65]

Critics say that monetary policy in the United States has not achieved consistent success in meeting the goals that have been delegated to the Federal Reserve System by Congress. Congress began to review more options with regard to macroeconomic influence beginning in 1946 (after World War II), with the Federal Reserve receiving specific mandates in 1977 (after the country suffered a period of stagflation).

Throughout the period of the Federal Reserve following the mandates, the relative weight given to each of these goals has changed, depending on political developments. In particular, the theories of Keynesianism and monetarism have had great influence on both the theory and implementation of monetary policy, and the "prevailing wisdom" or consensus view of the economic and financial communities has changed over the years.[66]

- Elastic currency (magnitude of the money multiplier): the success of monetary policy is dependent on the ability to strongly influence the supply of money available to the citizens. If a currency is highly "elastic" (that is, has a higher money multiplier, corresponding to a tendency of the financial system to create more broad money for a given quantity of base money), plans to expand the money supply and accommodate growth are easier to implement. Low elasticity was one of many factors that contributed to the depth of the Great Depression: as banks cut lending, the money multiplier fell, and at the same time the Federal Reserve constricted the monetary base. The depression of the late 1920s is generally regarded as being the worst in the country's history, and the Federal Reserve has been criticized for monetary policy which worsened the depression.[67] Partly to alleviate problems related to the depression, the United States transitioned from a gold standard and now uses a fiat currency; elasticity is believed to have been increased greatly.[68]

- High employment - Unemployment has experienced significant increases on occasion, despite the efforts of the Federal Reserve.[69] These periods include the early 1990s recession caused by the savings and loan crisis, the bursting of the dot-com bubble and the 2006 bursting of the housing bubble plus the 2007 subprime mortgage financial crisis. In some cases, the Federal Reserve intentionally sacrificed employment levels in order to rein in spiralling inflation, as was the case for the Early 1980s recession, which was induced to alleviate a stagflation problem.

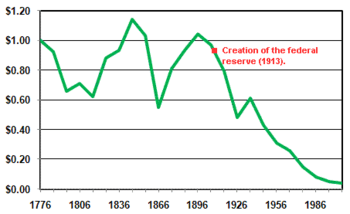

- Stable prices - While some economists would regard any consistent inflation as a sign of unstable prices,[71] policymakers could be satisfied with 1 or 2%;[72] the consensus of "price stability" constituting long-run inflation of 1-2% is, however, a relatively recent development, and a change that has occurred at other central banks throughout the world. Inflation has averaged a 4.22% increase annually following the mandates applied in 1977; historic inflation since the establishment of the Federal Reserve in 1913 has averaged 3.4%.[73] In contrast, some research indicates that average inflation for the 250 years before the system was near zero percent, though there were likely sharper upward and downward spikes in that timeframe as compared with more recent times.[74] Central banks in some other countries, notably the German Bundesbank, had considerably better records of achieving price stability drawing on experience from the two episodes of hyperinflation and economic collapse under the country's previous central bank.

Inflation worldwide has fallen significantly since former Federal Reserve Chairman Paul Volcker began his tenure in 1979, a period which has been called the Great Moderation; some commentators attribute this to improved monetary policy worldwide, particularly in the Organisation for Economic Co-operation and Development.[75][76] BusinessWeek notes that inflation has been relatively low since mid-1980s[77] and it was during this time that Volcker wrote (in 1995), "It is a sobering fact that the prominence of central banks [such as the Federal Reserve] in this century has coincided with a general tendency towards more inflation, not less. By and large, if the overriding objective is price stability, we did better with the nineteenth-century gold standard and passive central banks, with currency boards, or even with 'free banking.'".

- Sustainable growth - The growth of the economy may not be sustainable as the ability for households to save money has been on an overall decline[78] and household debt is consistently rising.[79]

Public confusion

The Federal Reserve has established a library of information on their websites, however, many experts have spoken about the general level of public confusion that still exists on the subject of the economy; this lack of understanding of macroeconomic questions and monetary policy, however, exists in other countries as well. Critics of the Fed widely regard the system as being "opaque", and one of the Fed's most vehement opponents of his time, Congressman Louis T. McFadden, even went so far as to say that "Every effort has been made by the Federal Reserve Board to conceal its powers...."[80]

There are, on the other hand, many economists who support the need for an independent central banking authority, and some have established websites that aim to clear up confusion about the economy and the Federal Reserve's operations. The Federal Reserve website itself publishes various information and instructional materials for a variety of audiences.

Criticism of government interference

Some economists, especially those belonging to the heterodox Austrian School, criticize the idea of even establishing monetary policy, believing that it distorts investment. Friedrich Hayek won the Nobel Prize for his elaboration of the Austrian business cycle theory.

Briefly, the theory holds that an artificial injection of credit, from a source such as a central bank like the Federal Reserve, sends false signals to entrepreneurs to engage in long-term investments due to a favorably low interest rate. However, the surge of investments undertaken represents an artificial boom, or bubble, because the low interest rate was achieved by an artificial expansion of the money supply and not by savings. Hence, the pool of real savings and resources have not increased and do not justify the investments undertaken.

These investments, which are more appropriately called "malinvestments," are realized to be unsustainable when the artificial credit spigot is shut off and interest rates rise. The malinvestments and unsustainable projects are liquidated, which is the recession. The theory demonstrates that the problem is the artificial boom which causes the malinvestments in the first place, made possible by an artificial injection of credit not from savings.

According to Austrian economics, without government intervention, interest rates will always be an equilibrium between the time-preferences of borrowers and savers, and this equilibrium is simply distorted by government intervention. This distortion, in their view, is the cause of the business cycle. Some Austrian economists - but by no means all - also support full reserve banking, a hypothetical financial/banking system where banks may not lend deposits. Others may advocate free banking, whereby the government abstains from any interference in what individuals may choose to use as money or the extent to which banks create money through the deposit and lending cycle.

Reserve requirement

The Federal Reserve regulates banking, and one regulation under its direct control is the reserve requirement which dictates how much money banks must keep in reserves, as compared to its demand deposits. Banks use their observation that the majority of deposits are not requested by the account holders at the same time.

Currently, the Federal Reserve requires that banks keep 10% of their deposits on hand.[81] Some countries have no nationally mandated reserve requirements—banks use their own resources to determine what to hold in reserve, however their lending is typically constrained by other regulations.[82] Other factors being equal, lower reserve percentages increases the possibility of Bank runs, such as the widespread runs of 1931. Low reserve requirements also allow for larger expansions of the money supply by actions of commercial banks—currently the private banking system has created much of the broad money supply of US dollars through lending activity. Monetary policy reform calling for 100% reserves has been advocated by economists such as: Irving Fisher,[83] Frank Knight,[84] many ecological economists along with economists of the Chicago School and Austrian School. Despite calls for reform, the nearly universal practice of fractional-reserve banking has remained in the United States.

Criticism of private sector involvement

Historically and to the present day, various social and political movements (such as Social credit) have criticized the involvement of the private sector in "creating money," claiming that only the government should have the power to "make money." Some proponents also support full reserve banking or other non-orthodox approaches to monetary policy. Various terminology may be used, including "debt money", which may have emotive or political connotations. These are generally considered to be akin to conspiracy theories by mainstream economists and ignored in academic literature on monetary policy.

See also

- Debt

- Free banking

- Hard currency

- History of monetary policy in the United States

- Monetarism

- Monetary policy

- Money supply

- Soft currency

- Treasury bills

References

- 1 2 "Archived copy". Archived from the original on 2014-05-28. Retrieved 2016-02-07. Paul Krugman, "Great Depression Blogging," January 17, 2008: "Monetary base only gets created or destroyed through Fed actions.

- ↑ Everett, Ray, Dr. "ECONOMICS: THEORY AND PRACTICE" (Seventh ed.). John Wiley & Sons, Inc. Retrieved 2008-01-11.

- 1 2 3 4 5 "A Case Study: The Federal Reserve System and Monetary Policy". Retrieved 2008-01-11.

As banks increase or decrease loans, the nation's money supply increases or decreases.

- ↑ Cacy, J. A. (November 1976). "Commercial Bank Loans and the Money Supply" (pdf). Monthly Review. Federal Reserve Bank of Kansas City: 3. Retrieved 2008-01-25.

Bank lending, however, is only one of several sources of potential increase in the narrowly defined money supply. Another source is the investing activity of commercial banks. As in the case of loans, when banks acquire investments, such as United States Government securities, the public may use the proceeds to augment its M1 balances. A third source of potential increase in money balances is the asset-acquiring activities of the Federal Reserve System. When the Federal Reserve buys U.S. Government securities, the proceeds potentially may be used by the public to add to its M1 balances.

- ↑ "Archived copy". Archived from the original on 2007-12-26. Retrieved 2008-02-03. Willem Buiter, Professor, London School of Economics, "Long Live Debt", Financial Times "Maverecon Blog", October 13, 2007. "

- ↑ Flaherty, Edward (2003-03-06). "A Brief History of Central Banking in the United States". Department of Humanities Computing. Retrieved 2008-02-01.

- ↑ "Is the Federal Reserve a privately owned corporation?". Federal Reserve Bank of San Francisco. Retrieved 2008-01-12.

the 12 Federal Reserve Banks are chartered as private corporations

- ↑ "Lewis v. United States, 680 F.2d 1239 (9th Cir. 1982)". Retrieved 2008-02-17.

The court stated "Examining the organization and function of the Federal Reserve Banks, and applying the relevant factors, we conclude that the Reserve Banks are not federal instrumentalities for purpose of the FTCA, but are independent, privately owned and locally controlled corporations."

- ↑ "Frequently Asked Questions: board of governors". Federal Reserve Bank of Richmond. Retrieved 2008-01-06.

- ↑ Federal Reserve Board, "The Federal Reserve System: Purposes and Functions". Archived June 15, 2013, at the Wayback Machine.

- ↑ STEVENSON, RICHARD W (1996-03-27). "Greenspan Calls the Fed 'Extraordinarily Well Run'". New York Times. Retrieved 2008-01-06.

- 1 2 Hassett, Kevin. "How the Fed Works". The American Enterprise Institute for Public Policy Research. Retrieved 2008-01-12.

- ↑ "FEDERAL RESERVE SYSTEM: The Surplus Account". United States General Accounting Office. Archived from the original on 2008-02-17. Retrieved 2008-01-12.

- ↑ "Archived copy". Archived from the original on 2016-04-07. Retrieved 2008-02-01. Edward Flaherty, Department of Economics, College of Charleston (S.C.), "Debunking the Federal Reserve Conspiracy Theories", Public Eye (Political Research Associates).

- ↑ "Reserve Requirements", Fedpoints, Federal Reserve Bank of New York

- ↑ "Archived copy". Archived from the original on 2016-08-20. Retrieved 2011-08-29. "Federal Funds", Fedpoints, Federal Reserve Bank of New York

- ↑ "Reserve requirements", Fedpoints, Federal Reserve Bank of New York

- ↑ "How Currency Gets into Circulation". Federal Reserve Bank of New York. Retrieved 2008-01-06.

- ↑ "Money Stock Measures". Federal Reserve, Board of Governors. Retrieved 2008-01-06.

- ↑ Schenk, Robert, Ph.D. "From Commodity to Bank-Debt Money". Retrieved 2008-01-07.

Professor of Economics

- ↑ "Reserve Requirements". Retrieved 2008-01-07.

- ↑ "Frequently Asked Questions about the Public Debt". U.S. Department of the Treasury, Bureau of the Public Debt. Retrieved 2008-01-06.

- ↑ "The Federal Reserve's Beige Book". The Federal Reserve Bank of Minneapolis. Retrieved 2008-01-06.

- ↑ "The Federal Reserve, Monetary Policy and the Economy". The Federal Reserve Bank of Dallas. Retrieved 2008-01-06.

- ↑ Davies, Phil. "Right on Target". Retrieved 2008-01-07.

Federal Reserve Bank of Minneapolis

- 1 2 "Open Market Operations". Federal Reserve Bank of New York. Retrieved 2008-01-11.

Open market operations enable the Federal Reserve to affect the supply of reserve balances in the banking system.

- 1 2 "The First 90 Years of the Federal Reserve Bank of Boston". Federal Reserve Bank of Boston. Archived from the original on November 17, 2007. Retrieved 2008-01-11.

Open market operations become the primary tool for carrying out monetary policy, with discount rate and reserve requirement changes used as occasional supplements.

- 1 2 "Reserve Requirements". Retrieved 2008-01-10.

Federal Reserve Bank of New York

- 1 2 Schwartz, Anna J. "Money Supply". The Concise Encyclopedia of Economics. Retrieved 2008-01-11.

If the Federal Reserve increases reserves, a single bank can make loans up to the amount of its excess reserves, creating an equal amount of deposits

- 1 2 3 Simons, Howard L. "Don't Blame (or Credit) the Fed". Retrieved 2008-01-11.

The Federal Reserve's open market operations affect the level of free reserves in the banking system. It is the lending of these free reserves throughout the banking system that expands the supply of credit.

- 1 2 3 4 Nichols, Dorothy M (May 1961). Modern Money Mechanics. Federal Reserve Bank of Chicago. p. 3. Archived from the original (PDF) on 2008-01-11. Retrieved 2008-01-11.

The actual process of money creation takes place primarily in banks. As noted earlier, checkable liabilities of banks are money. These liabilities are customers' accounts. They increase when customers deposit currency and checks and when the proceeds of loans made by the banks are credited to borrowers' accounts.

- 1 2 "MONEY MULTIPLIER". Retrieved 2008-01-11.

... borrowers are also inclined to convert checkable deposits into currency.

- ↑ "Fact Sheets: Currency & Coins". United States Department of the Treasury. Retrieved 2008-01-22.

- ↑ "Money Facts". United States Treasury, Bureau of Engraving and Printing. Archived from the original on September 28, 2007. Retrieved 2008-01-06.

- ↑ Federal Reserve Bank of New York, 2007 Annual Report Archived October 19, 2012, at the Wayback Machine., Note h: Federal Reserve Notes (p. 12): "The Federal Reserve Act provides that the collateral security tendered by the Reserve Bank ... must be at least equal to the sum of notes applied for by such Reserve Bank."

- ↑ Schenk, Robert E., Ph.D. "From Commodity to Bank-Debt Money". Retrieved 2008-01-11.

Money creation was a by-product of the making of the loan.

- ↑ Marshall, David. "Origins of the use of Treasury debt in open market operations: Lessons for the present" (PDF). Federal Reserve Bank of Chicago. p. 2. Archived from the original (PDF) on 2008-05-29. Retrieved 2008-02-04.

Thus, to a close approximation, every dollar's worth of M0 in circulation is matched on the Fed's balance sheet by one dollar's worth of U.S. Treasury securities acquired through open market purchases.

- 1 2 Mings, Turley; Marlin, Matthew. "The Study of Economics: Principles, Concepts & Applications" (Sixth ed.). The McGraw-Hill Companies.

- ↑ Cunningham, Steve, Ph.D. "ECON 111 Principles of Macroeconomics: Lecture Notes". Kent State University. Archived from the original (– Scholar search) on 2008-05-29. Retrieved 2008-01-07.

- ↑ Roy, Udayan. "Introduction to Economics". Long Island University. Retrieved 2008-01-12.

Ultimately all of the newly printed cash must end up as required reserves.

- 1 2 3 4 Daly, Herman. "Ecological Economics: The Concept of Scale and Its Relation to Allocation, Distribution, and Uneconomic Growth" (PDF). University of Maryland. Archived from the original (PDF) on 2006-09-21. Retrieved 2008-01-11.

- ↑ "How Currency Gets into Circulation". Federal Reserve Bank of New York. Retrieved 2008-01-11.

Virtually all of currency notes in use are Federal Reserve notes.

- ↑ "Who are the largest holders of U.S. public debt?". Federal Reserve Bank of San Francisco. Archived from the original on July 8, 2006. Retrieved 2008-01-06.

- ↑ Thomas Palley, "The Case Against Budget Surpluses Archived April 13, 2016, at the Wayback Machine.," Challenge, Nov. - Dec., 2001, 13 - 27: "...the interest rate payable on government debt establishes the pure risk free interest rate that provides a benchmark for the entire system."

- ↑ "What will happen to the Fed if the national debt is paid off?". Federal Reserve Bank of San Francisco. Archived from the original on 2008-05-26. Retrieved 2008-01-06.

- ↑ Joseph H. Haslag, 1998. "Seigniorage revenue and monetary policy: some preliminary evidence Archived July 17, 2012, at the Wayback Machine.," Economic and Financial Policy Review, Federal Reserve Bank of Dallas, issue Q III, pages 10-20.

- ↑ Daly, Herman E (2007). Ecological Economics and Sustainable Development, Selected Essays of. Edward Elgar Publishing. ISBN 1-84720-101-6.

- ↑ Miller, Eric (August 27, 2004). "A Treatise on the Ecological Economics of Money" (PDF). York University: 72. Archived from the original (pdf) on July 15, 2007. Retrieved 2008-01-26.

The growth of fractional-reserve fiat money is better understood as a response to the financing needs of economic activities, not the cause of those activities.

- ↑ Calvo, Guillermo A; Reinhart, Carmen M. "When Capital Inflows Come to a Sudden Stop: Consequences and Policy Options" (PDF). International Monetary Fund: 20. Retrieved 2008-02-04.

- ↑ McConnell, C.; Brue, S. (2005). Microeconomics: Principles, Problems, and Policies. McGraw-Hill Professional. p. 303. ISBN 0-07-287561-5. Retrieved 2008-02-06..

- ↑ Schmitt, Elizabeth Dunne. "Myths vs. Realties for the United States Federal Reserve System". Retrieved 2008-01-09.

Professor of Economics

- ↑ BoG 2005, pp. 18–21

- ↑ Joseph Mason, Ali Anari, and James Kolari, "THE STOCK OF CLOSED BANK DEPOSITS, DURATION OF CREDIT CHANNEL EFFECTS, AND THE PERSISTENCE OF THE U.S. GREAT DEPRESSION" Archived June 9, 2011, at the Wayback Machine.: "Since Ben Bernanke's (1983) seminal paper entitled "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression"...

- ↑ "Financial Instability and the Federal Reserve as a Liquidity Provider". Archived from the original on October 11, 2006. Retrieved 2008-01-06.

- ↑ Stiglitz, Joseph (5 November 2010). "New $600B Fed Stimulus Fuels Fears of US Currency War". Democracy Now. Retrieved 5 November 2010.

- ↑ Wheatley, Jonathan; Peter Garnham (5 November 2010). "Brazil in 'currency war' alert". Financial Times. Retrieved 5 November 2010.

- ↑ FRB: OIG - Mission Archived April 11, 2009, at the Wayback Machine.

- ↑ FRB: OIG - Complete List of OIG Reports - 2007 Archived October 2, 2013, at the Wayback Machine.

- ↑ "THE FEDERAL RESERVE BOARD (Senate - March 26, 1996)". Retrieved 2008-01-06.

- 1 2 "Archived copy" (PDF). Archived (PDF) from the original on 2016-03-03. Retrieved 2008-02-02. Charles Bowsher, "Federal Reserve System Audits: Restrictions on GAO's Access", Statement by Charles Bowsher, Comptroller General of the United States, October 27, 1993.

- 1 2 3 Smale, Pauline. "Structure and Functions of The Federal Reserve System" (PDF). Congressional Research Service. p. 6. Archived from the original (PDF) on 2008-02-01. Retrieved 2008-02-01.

- ↑ UCHITELLE, LOUIS (1989-08-24). "Moves On in Congress to Lift Secrecy at the Federal Reserve". New York Times. Archived from the original on 2008-01-15. Retrieved 2008-01-06.

- ↑ "Archived copy". Archived from the original on 2012-02-18. Retrieved 2008-02-02. Federal Reserve Act, Section 11b ([12 USC 248b.]).

- ↑ Havrilesky, Thomas M. (1995). The Pressures on American Monetary Policy. Springer; ISBN 0-7923-9561-1. p. 113. ISBN 978-0-7923-9561-4. Retrieved 2008-02-01.

- ↑ "Monetary Policy". Federal Reserve Bank of New York. Archived from the original on December 8, 2007. Retrieved 2008-01-06.

- ↑ "Archived copy". Archived from the original on 2012-11-14. Retrieved 2016-05-18. Allan H. Metzler, A History of the Federal Reserve.

- ↑ Bernanke, Ben S. "Money, Gold, and the Great Depression". Federal Reserve Board. Retrieved 2008-01-06.

Governor, Federal Reserve

- ↑ "The Evolution of Banking in a Market Economy". Retrieved 2008-02-06.

- ↑ "Business Cycle Expansions and Contractions". National Bureau of Economic Research, Inc. Archived from the original on 2007-10-12. Retrieved 2008-02-06.

- ↑ Purchasing Power of Money in the United States from 1774 to 2006 Archived July 19, 2016, at the Wayback Machine. from measuringworth.com

- ↑ "Low Inflation or No Inflation". Retrieved 2008-01-06.

- ↑ Anderson, Richard G (2006). "Inflation's Economic Cost: How Large? How Certain?". Federal Reserve Bank of St. Louis - Regional Economist. Retrieved 2008-01-06.

Vice President, Federal Reserve Bank of St. Louis

- ↑ "Consumer Price Index, 1913-". Federal Reserve Bank of Minneapolis. Archived from the original on 2007-08-12. Retrieved 2008-01-06.

- ↑ Sahr, Robert. "Inflation Conversion Factors for Dollars 1665 to Estimated 2017". Retrieved 2008-01-06.

Assoc. Professor of Political Science

- ↑ John Taylor, "Monetary Policy and the Long Boom" Archived October 11, 2016, at the Wayback Machine., Federal Reserve Bank of St. Louis Review, November–December 1998.

- ↑ Peter M. Summers, "What Caused the Great Moderation? Some Cross-Country Evidence" Archived October 31, 2013, at the Wayback Machine., Kansas City Federal Reserve Bank: "The most common explanations for increased output stability include better monetary policy."

- ↑ Ghosh, Palash R. "Investor TIPS for Fighting Inflation".

The annual inflation rate has been relatively low since the mid-1980s

- ↑ "Personal Saving Rate". U.S. Department of Commerce, Bureau of Economic Analysis. Retrieved 2008-01-06.

- ↑ Hodges, Michael W. "Grandfather Economic Report series". Retrieved 2008-01-06.

- ↑ "AN ASTOUNDING EXPOSURE". Retrieved 2008-01-06.

- ↑ "Board of the Governors of the Federal Reserve System".

In April 2007, the reserve requirement was 10% on transaction deposits and 0% on time deposits

- ↑ "Archived copy". Archived from the original on 2016-03-04. Retrieved 2013-09-15. Kevin Clinton, Bank of Canada: "Implementation of Monetary Policy in a Regime with Zero Reserve Requirements", Bank of Canada Working Paper 97–8, 1997. "A number of countries now have no requirement, such as Australia, Belgium, Canada, Sweden and the United Kingdom."

- ↑ Fisher, Irving (1997). 100% Money. Pickering & Chatto Ltd;. ISBN 978-1-85196-236-5.

- ↑ Daly, Herman E; Farley, Joshua (2004). Ecological Economics: Principles and Applications. Island Press. p. 250. ISBN 1-55963-312-3.

External links

- Board of Governors of the Federal Reserve System

- Federal Reserve Bank of New York

- Savings rate viz Fed rate from 1954 Historical relationship between the savings rate and the Fed rate - since 1954

- USA Fed rate behavior under various presidencies since 1954

- Wages and Benefits: Real Wages (1964–2004)