Single Euro Payments Area

| Single Euro Payments Area |

||

|---|---|---|

|

||

| Official languages | ||

| Member states | 34 states

|

|

| Area | ||

| • | Total | 4,854,382 km2 1,874,287 sq mi |

| Population | ||

| • | 2011 census | 516,881,997 |

| • | Density | 106.5/km2 275.8/sq mi |

| GDP (PPP) | estimate | |

| • | Total | $11,465 billion (2012)[1] |

| • | Per capita | $34,583 (2012)[1] |

| Time zone | UTC, CET, EET (UTC±0 to +2) | |

| • | Summer (DST) | WEST, CEST, EEST (UTC+1 to +3) |

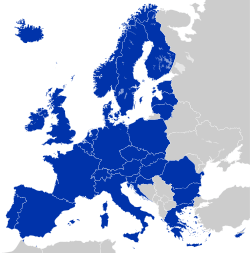

The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers denominated in euro. As of July 2015, SEPA consists of the 28 member states of the European Union, the four member states of the European Free Trade Association (Iceland, Liechtenstein, Norway and Switzerland), Monaco and San Marino.[2]

Goals

The project's aim is to improve the efficiency of cross-border payments and turn the fragmented national markets for euro payments into a single domestic one. SEPA will enable customers to make cashless euro payments to anyone located anywhere in the area, using a single bank account and a single set of payment instruments.[3] People who have a bank account in a eurozone country, will be able to use it to receive salaries and make payments all over the eurozone, for example when they take a job in a new country.

The project includes the development of common financial instruments, standards, procedures, and infrastructure to enable economies of scale. This should, in turn, reduce the overall cost to the European economy of moving capital around the region (estimated as two to three percent of total GDP).[4]

Overview

There are two milestones in the establishment of SEPA:

- Pan-European payment instruments for credit transfers began on 28 January 2008; direct debits and debit cards became available later

- By the end of 2010, all present national payment infrastructures and payment processors were expected to be in full competition to increase efficiency through consolidation and economies of scale

For direct debits, the first milestone was missed due to a delay in the implementation of enabling legislation (the Payment Services Directive or PSD) in the European Parliament. Direct debits became available in November 2009, which put time pressure on the second milestone.[5]

The European Commission has established the legal foundation through the PSD. The commercial and technical frameworks for payment instruments were developed by the European Payments Council (EPC), made up of European banks. The EPC is committed to delivering three pan-European payment instruments:

- Credit transfers: SCT – SEPA Credit Transfer

- Direct debits: SDD – SEPA Direct Debit. Banks began offering this service on 2 November 2009.[6]

- Cards: SEPA Cards Framework

To provide end-to-end straight through processing (STP) for SEPA-clearing, the EPC committed to delivering technical validation subsets of ISO 20022. Whereas bank-to-bank messages (pacs) are mandatory for use, customer-to-bank Payment Initialization (PAIN) message types are not; however, they are strongly recommended. Because there is room for interpretation, it is expected that several PAIN specifications will be published in SEPA countries.

Businesses, merchants, consumers and governments are also interested in the development of SEPA. The European Associations of Corporate Treasurers (EACT), TWIST, the European Central Bank, the European Commission, the European Payments Council, the European Automated Clearing House Association (EACHA), payments processors and pan-European banking associations – European Banking Federation (EBF), European Association of Co-operative Banks (EACB) and the European Savings Banks Group (ESBG) – are playing an active role in defining the services which SEPA will deliver.

Since January 2008, banks have been switching customers to the new payment instruments. By 2010, the majority were expected to be on the SEPA framework. As a result, banks throughout the SEPA area (not just the Eurozone) need to invest in technology with the capacity to support SEPA payment instruments.

SEPA clearance is based on the IBAN bank-account identification and the SWIFT-BIC bank identifier. Domestic euro transactions are routed by IBAN; earlier national-designation schemes were abolished by February 2014, providing uniform access to the new payment instruments. Since February 2016 Eurozone consumers must drop BIC sorting information for SEPA transactions, it is derived from the IBAN for all banks in the SEPA area.

An instant payment scheme named SCTinst is scheduled to be implemented by November 2017.[7]

SEPA covers only normal bank transfers. Payment methods which have additional optional features or services, such as mobile phone or smart card payment systems, are not directly covered.[8]

There are no short term plans of extending SEPA to payments made in the currencies of the non-euro SEPA countries. People and businesses who live in those countries have often the option of getting a euro account from their local bank if they have transactions in euro or plan to settle in a Eurozone country. People from the eurozone can use their bank account all over the zone but still need a local bank account if they work in a non-euro SEPA country.

Coverage

SEPA consists of 34 countries:[2]

- The 28 member states of the European Union, including

- the 19 states that are in the Eurozone:

- the nine states that are not in the Eurozone:

- Bulgaria, Croatia, the Czech Republic, Denmark, Hungary, Poland, Romania, Sweden, United Kingdom.

- The three states having signed the European Economic Area agreement:

- A few other countries with agreements with the EU:

All parts of a country are normally part of SEPA. However, the following countries have special territories which are not part of SEPA:

- Cyprus: Northern Cyprus is excluded.

- Denmark: the Faroe Islands and Greenland are excluded.

- France: the French Southern and Antarctic Lands, French Polynesia, New Caledonia and Wallis and Futuna are excluded. Nevertheless, the 3 last are part of SEPA COM Pacifique.

- Netherlands: Aruba, the Caribbean Netherlands, Curaçao and Sint Maarten are excluded.

- Norway: Svalbard is excluded.

- United Kingdom: The British Overseas Territories are excluded,[9] but Gibraltar and the Crown dependencies are included.

Jurisdictions using the euro that are not included: Akrotiri and Dhekelia, Kosovo, Montenegro, Andorra and Vatican City.[9]

Charges

SEPA guarantees that euro payments are received within a guaranteed time, and banks are not allowed to make any deductions of the amount transferred, introduced by a regulation in year 2001.[10] Banks and payment institutions still have the option of charging a credit-transfer fee of their choice for euro transfers if it is charged uniformly to all EEA participants, banks or payment institutions, domestic or foreign.[11] This is relevant for countries which do not use the euro; domestic transfers in euro by consumers are uncommon, and inflated fees might be charged. Sweden and Denmark have legislated that euro transfers shall be charged the same as transfers in their own currency; which has the effect of giving free euro ATM withdrawals, but charges for ATM withdrawals in other currencies used in the EU.

In Regulation (EC) 924/2009, the European Parliament mandated that charges in respect of cross-border payments in euro (of up to EUR 50,000) to other Member States shall be the same as the charges for corresponding national payments.[12][13] However, the EU Regulation does not apply to all SEPA countries; the most significant difference is the inclusion of Switzerland in SEPA but not the EU. The rule of the same price applies, even if the transaction is sent as an international transaction instead of a SEPA transaction (common before 2008, or if any involved bank does not support SEPA transactions). The regulation 924/2009 does not regulate charges for currency conversion so charges for non-euro transactions can still be applied (if not banned by national law).[14]

Key dates

| 1957 | Treaty of Rome creates the European Community |

|---|---|

| 1992 | Maastricht Treaty creates the euro |

| 1999 | Introduction of the euro as an electronic currency, including introduction of the RTGS system TARGET for large-value transfers |

| 2000 | Lisbon Strategy: Meeting creates European Financial Services Action Plan |

| 2001 | EC Regulation 2560/2001 harmonises fees for cross-border and domestic euro transactions[11] |

| 2002 | Introduction of Euro banknotes and coins |

| 2003 | First pan-European ACH (PE-ACH) goes live; EC Regulation 2560/2001 comes into force for transactions up to €12,500 |

| 2006 | EC Regulation 2560 cap increases euro transactions up to €50,000 |

| 2008 | SEPA pan-European payment instruments become operational (parallel to domestic instruments) on 28 January[15] |

| 2009 | Payment Services Directive (PSD) enacted in national laws by November |

| 2010 | SEPA payments become dominant form of electronic payments |

| 2011 | SEPA payments replace national payments in the Eurozone |

| 2014 | 1 August: Single Euro Payments Area (SEPA) becomes fully operational in all Eurozone countries.[16] |

| 2016 | Since 31 October 2016, payment service providers in non-euro countries are only able to collect euro-denominated payments using SEPA procedures. Non-Euro schemes, such as UK Direct Debit, will continue without change.[17] |

Uptake

As of August 2014, 99.4% of credit transfers, 99.9% of direct debit and 79.2% of card payments have been migrated to SEPA in the euro area.[18]

The official progress report was published in March 2013.[19]

In October 2010, the European Central Bank published its seventh progress report on SEPA.[20] The European Central Bank regards SEPA as an essential element to advance the usability and maturity of the euro.

See also

References

- 1 2 "5. Report for Selected Countries and Subjects". International Monetary Fund. 17 June 2011. Retrieved 10 July 2013.

- 1 2 List of SEPA Scheme Countries

- ↑ "Solution: SEPA, the single euro payments area". European Central Bank. Archived from the original on 20 March 2008. Retrieved 28 January 2008.

- ↑ "Agreement reached on cross-border banking". RTÉ News. 27 March 2007. Retrieved 28 January 2008.

- ↑ "Joint statement by the European Commission and the European Central Bank welcoming the European Parliament's adoption of the Payment Services Directive". Europa (web portal) (Press release). European Union. 24 April 2007. Archived from the original on 19 May 2011. Retrieved 26 April 2011.

- ↑ EUROPA – Press Releases – Single Euro Payments Area (SEPA): cross-border direct debits now a reality EUROPA (European Union), 3 November 2009; Retrieved 4 February 2011

- ↑ Instant payments

- ↑ REGULATION (EU) No 260/2012 (article 1 point 3)

- 1 2 "The Boundaries of SEPA-land" (PDF). Skandinaviska Enskilda Banken. 9 April 2013. Retrieved 26 June 2013. Archived 26 June 2013 at the Wayback Machine.

- ↑ Single Euro Payments Area (SEPA) – frequently asked questions. Brussels, 31 July 2014.

- 1 2 Regulation (EC) No 2560/2001 of the European Parliament and the Council of the European Union EUR-Lex, 19 December 2001

- ↑ Cross-border payments in euro: Regulation on equality of charges, European Commission European Commission, 19 September 2013

- ↑ Regulation (EC) No 924/2009 of the European Parliament and of the Council of 16 September 2009 on cross-border payments in the Community and repealing Regulation (EC) No 2560/2001 EUR-Lex, 9 October 2009

- ↑ Regulation (EC) No 924/2009 ... Frequently Asked Questions (FAQ) (see point 9)

- ↑ "Single Euro Payments Area kicks in, EU – European Information on Financial Services". EurActiv.com. 28 January 2008. Retrieved 26 April 2011.

- ↑ Vice-President Michel Barnier welcomes major milestone for the internal payments market with the migration to SEPA (Single Euro Payments Area). Brussels, 1 August 2014.

- ↑ "Migrating to the Single Euro Payments Area: key facts". European Central Bank. Retrieved 15 August 2016.

- ↑ ECB. Key figures: SEPA indicators at a glance (euro area).

- ↑ "Quantitative indicators" (PDF). European Central Bank. March 2013. Retrieved 26 May 2013.

- ↑ "Single Euro Payments Area Seventh Progress Report: Beyond Theory into Practice" (PDF). European Central Bank. October 2010. Retrieved 26 May 2013.

External links

- Official website

- SEPA on ECB website (and per-country links)

- European Payments Council (EPC), representing the European banking industry

- REGULATION (EU) No 260/2012 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 14 March 2012 - establishing technical and business requirements for credit transfers and direct debits in euro and amending Regulation (EC) No 924/2009 Official Journal of the European Union, 30 March 2012 - European Regulation 260/2012 establishing technical and business requirements for credit transfers and direct debits in euro

- SEPA Payments News & Views for Corporates

Euro topics | |||||||

|---|---|---|---|---|---|---|---|

| General | |||||||

| Administration | |||||||

| Fiscal provisions | |||||||

| History | |||||||

| Economy | |||||||

| International status | |||||||

| Denominations | |||||||

| Coins by issuing country |

| ||||||

Potential adoption by other countries |

| ||||||

| Currencies yielded |

| ||||||

| |||||||

| |||||||