Sustainable Value

Sustainable value is a way of managing and measuring sustainability performance. The concept was developed by researchers who are working today for Euromed Management School (Marseille/France) and the IZT - Institute for Futures Studies and Technology Assessment (Berlin/Germany). To date Sustainable Value is primarily used to assess corporate sustainability performance.

Sustainable value differs from existing approaches by the fact that it is value-based while all other existing approaches to sustainability assessment (such as environmental impact assessments) are burden-based, i.e. they are assessing environmental and social resource use based on the burden that is created. Using the sustainable value approach, economic, environmental and social resources are assessed and aggregated based on their relative value contribution and can be expressed in a monetary unit like euros, dollars or pounds.

The concept

Sustainable value is based on the notion of opportunity costs. Opportunity costs are used in financial markets to calculate the cost of capital. In financial markets, the cost of using € 100 over the course of one year is determined by the return that could have been generated through an alternative investment of the capital. Sustainable Value is the first concept to extend this logic to environmental and social resources.

Sustainable value is calculated in five steps:

- Calculate the environmental, social and economic efficiencies of the entity using the resources. Efficiency is calculated by relating the return to resource use.

- Calculate the environmental, social and economic efficiencies of the benchmark (= calculate opportunity costs).

- Calculate the value spreads by subtracting the efficiency of the benchmark (Step 2) from the efficiency of the entity (Step 1).

- Calculate the value contributions by multiplying the amount of environmental, social and economic resources used with the corresponding value spread (Step 3), respectively.

- Calculate sustainable value by adding up the value contributions (Step 4) and dividing by the number of resources considered. This avoids double counting.

Sample application

The sustainable value approach can be demonstrated using the example of British Petroleum (BP) (For a detailed explanation see Figge, F. & Hahn, T. (2005): "The Cost of Sustainability Capital and the Creation of Sustainable Value by Companies", Journal of Industrial Ecology, 9(4), 47-58.).

In 2001, BP created the following return and employed the following economic, environmental and social resources (Table 1):

Table 1: Performance data of BP in 2001

| BP (2001) | Amount |

| Net Value Added [£ million] | 15,563 |

| Nonfinancial Assets [£ million] | 69,885 |

| CO2 [t] | 73,420,000 |

| CH4 [t] | 367,201 |

| SO2 [t] | 224,541 |

| NOx [t] | 266,133 |

| CO [t] | 124,584 |

| Work accidents [number] | 83 |

| PM10 [t] | 16,666 |

Note: t = metric tonne = megagram (Mg) = 1000 kilograms (kg, SI) ≈ 1.102 short tons

Source: Figge & Hahn 2005

In this example the return of BP is measured as Net Value Added and the UK economy is used as a benchmark. The macroeconomic equivalent of Net Value Added is the Net Domestic Product (NDP). Table 2 shows the Net Domestic Product and resource use of the UK economy in 2001.

Table 2: Performance data of the United Kingdom in 2001

| UK economy (2001) | Amount |

| Net Domestic Product [£ million] | 884,718 |

| Total Net Wealth [£ million] | 4,375,200 |

| CO2 [t] | 572,500,000 |

| CH4 [t] | 2,195,238 |

| SO2 [t] | 1,125,000 |

| NOx [t] | 1,680,000 |

| CO [t] | 3,966,500 |

| Work accidents [number] | 132,696 |

| PM10 [t] | 178,000 |

Source: Figge & Hahn (2005)

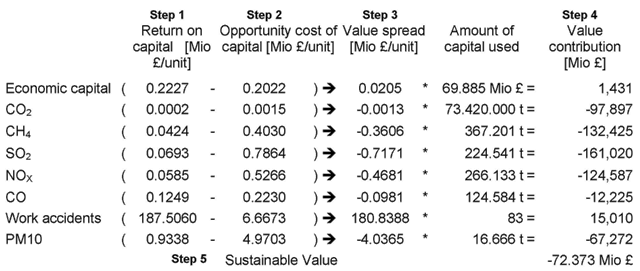

The next table shows how Sustainable Value is calculated.

As described above, in the first step the return on resources of BP is calculated.

BP generated about £ 212 Net value Added per ton of CO2 in 2001.

In a second step the return on resources of the UK economy (benchmark) is calculated.

The UK economy generated about £ 1,545 Net Domestic Product per ton of CO2 in 2001.

In a third step the value spread is calculated.

In 2001, BP generated £ 1,333 less return than the UK economy per ton of CO2.

In a fourth step the value contribution is calculated.

In 2001, the use of 73,420,000 t of CO2 generated about £98bn less return than if CO2 had been given to the UK economy on average. This step is repeated for all resources employed by the company.

In a fifth step all value contribution are added up and divided by the number of resources considered. The result is called Sustainable Value.

Table 3: Calculation of BP’s Sustainable Value for the year 2001

Source: Figge & Hahn 2005

BP’s Sustainable Value amounts to about £72bn. Put differently, had BP’s set of financial, environmental and social resources been used by the UK economy on average rather than by BP an additional £72bn Net Domestic Product could have been created.

Projects

The Sustainable value approach has been applied in several projects and case studies.

The EU-funded project ADVANCE (Application and Dissemination of Value-based Eco-ratings financial markets) used the Sustainable Value approach to assess the environmental performance of 65 European companies in monetary terms.

In a project that is funded by the German Federal Ministry of Education and Research (NeW – Nachhaltig erfolgreich Wirtschaften) the Sustainable Value approach is used to assess the triple bottom line performance of 28 German companies.

In a new EU-funded project SVAPPAS (Sustainable Value Analysis of Policy and Performance in the Agricultural Sector) a European consortium of research organisations uses the Sustainable Value approach to measure the sustainability performance of the agricultural sector in Europe.

See also

References

- Figge, F. & Hahn, T. (2006) "Looking for Sustainable Value", Environmental Finance, 7(8), 34-35

- Figge, F. & Hahn, T. (2005) "The Cost of Sustainability Capital and the Creation of Sustainable Value by Companies", Journal of Industrial Ecology, 9(4), 47-58.

- Figge, F. & Hahn, T. (2004) "Value-oriented impact assessment: the economics of a new approach to impact assessment", Journal of Environmental Planning and Management, 47(6), 921-941.

- Figge, F. & Hahn, T. (2004) "Sustainable Value Added: Measuring Corporate Contributions to Sustainability Beyond Eco-Efficiency", Ecological Economics, 48(2), 173-187.

- Van Passel, S., Nevens, F., Mathijs, E. & Van Huylenbroeck, G. (forthcoming) "Measuring farm sustainability and explaining differences in sustainable efficiency", Ecological Economics.

External links

- Methodological website: www.SustainableValue.com

- Sustainable Value Calculator: www.SustainableValueCalculator.com

- ADVANCE project website: www.advance-project.org

- SVAPPAS project website: www.svappas.ugent.be