Enlargement of the eurozone

The enlargement of the eurozone is an ongoing process within the European Union (EU). All member states of the European Union, except Denmark and the United Kingdom which negotiated opt-outs from the provisions, are obliged to adopt the euro as their sole currency once they meet the criteria, which include: complying with the debt and deficit criteria outlined by the Stability and Growth Pact, keeping inflation and long-term governmental interest rates below certain reference values, stabilizing their currency's exchange rate versus the euro by participating in the European Exchange Rate Mechanism (ERM II), and ensuring that their national laws comply with the ECB statute, ESCB statute and articles 130+131 of the Treaty on the Functioning of the European Union. The obligation for EU member states to adopt the euro was first outlined by the Maastricht Treaty of 1992, which became binding on all new member states by the terms of their treaties of accession.

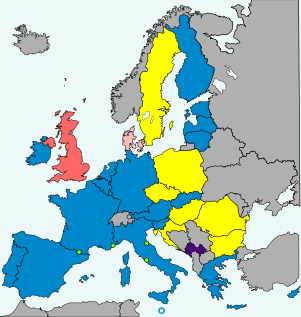

As of 2016, there are 19 EU member states in the eurozone, of which the first 11 (Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Portugal and Spain) introduced the euro on 1 January 1999 when it was electronic only. Greece joined 1 January 2001, one year before the physical euro coins and notes replaced the old national currencies in the eurozone. Subsequently, the following seven countries also joined the eurozone on 1 January in the mentioned year: Slovenia (2007), Cyprus (2008), Malta (2008), Slovakia (2009),[1] Estonia (2011),[2] Latvia (2014)[3] and Lithuania (2015).

Seven remaining states are on the enlargement agenda: Bulgaria, Croatia, Czech Republic, Hungary, Poland, Romania and Sweden. Denmark is not obliged to join, though should the country decide to do so it may join the eurozone with little difficulty as Denmark is already part of the ERM-II. The United Kingdom has opted to stay outside of the EMU, and currently has no intention of adopting the euro, rather it held a referendum on continuing to be a member of the EU at all, which resulted in a 51.9%-majority vote in favour of the UK's leaving the EU.[4][5][6][7]

Accession procedure

All EU members which have joined the bloc since the signing of the Maastricht treaty in 1992 are legally obliged to adopt the euro once they meet the criteria, since the terms of their accession treaties make the provisions on the euro binding on them. In order for a state to formally join the eurozone, enabling them to mint euro coins and get a seat at the European Central Bank (ECB) and the Eurogroup, a country must be a member of the European Union and comply with five convergence criteria, which were initially defined by the Maastricht Treaty in 1992. These criteria include: complying with the debt and deficit criteria outlined by the Stability and Growth Pact, keeping inflation and long-term governmental interest rates below reference values, and stabilizing their currency's exchange rate versus the euro. Generally, it is expected that the last point will be demonstrated by two consecutive years of participation in the European Exchange Rate Mechanism (ERM II),[8] though according to the Commission "exchange rate stability during a period of non-participation before entering ERM II can be taken into account."[9] The country must also ensure that their national laws are compliant with the ECB statute, ESCB statute and articles 130+131 of the Treaty on the Functioning of the European Union.

Since the convergence criteria require participation in the ERM, and non-eurozone states are responsible for deciding when to join ERM, they can ultimately control when they adopt the euro by staying outside the ERM and thus deliberately failing to meet the convergence criteria until they wish to. In some non-eurozone states without an opt-out, there has been discussion about holding referendums on approving their euro adoption.[10][11][12][13][14][15][16][17][18] Of the 16 states which have acceded to EU since 1992, the only state to have staged a euro referendum to date is Sweden, which in 2003 rejected its government's proposal to adopt the euro in 2006.

The European microstates of Monaco, San Marino and the Vatican City, which are not members of the EU but had a monetary agreement with a eurozone state when the euro was introduced, were granted a special permission to continue these agreements and to issue separate euro coins, but they don't get any input or observer status in the economic affairs of the eurozone. Andorra, which had used the euro unilaterally since the inception of the currency, negotiated a similar agreement which granted it the right to officially use the euro as of 1 April 2012 and to mint euro coins.[19]

In 2009 the authors of a confidential International Monetary Fund (IMF) report suggested that in light of the ongoing global financial crisis, the EU Council should consider granting EU member states which are having difficulty complying with all five convergence criteria the option to "partially adopt" the euro, along the lines of the monetary agreements signed with the microstates outside the EU. These states would gain the right to adopt the euro and issue a national variant of euro coins, but would not get a seat in ECB or the Eurogroup until they met all the convergence criteria.[20] However, the EU has not made use of this alternative accession process.

Current convergence status

| Convergence criteria (valid for the compliance check conducted by ECB in their June 2016 Report) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | HICP inflation rate[21][nb 1] | Excessive deficit procedure[22] | Exchange rate | Long-term interest rate[23][nb 2] | Compatibility of legislation | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Budget deficit to GDP[24] | Debt-to-GDP ratio | ERM II member[25] | Change in rate[26][27][nb 3] | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Reference values[nb 4] | Max. 0.7%[nb 5] Additionally, if the debt-to-GDP ratio exceeds 60% but is "sufficiently diminishing and approaching the reference value at a satisfactory pace" it can be deemed to be in compliance.[33]

Criterion not fulfilled

Reference values for the HICP criteria and interest rate criteriaThe compliance check above was conducted in June 2014, with the HICP and interest rate reference values specifically applying for the last assessment month with available data (April 2014). As reference values for HICP and interest rates are subject for monthly changes, any EU member state with a euro derogation has the right to ask for a renewed compliance check at any time during the year. For this potential extra assessment, the table below feature Eurostat's monthly publication of values being used in the calculation process to determine the reference value (upper limit) for HICP inflation and long-term interest rates, where a certain fixed buffer value is added to the moving unweighted arithmetic average of the three EU Member States with the lowest HICP inflation rates (ignoring states classified as "outliers"). The black values in the table are sourced by the officially published convergence reports, while the lime-green values are only qualified estimates, not confirmed by any official convergence report but sourced by monthly estimation reports published by the Polish Ministry of Finance. The reason why the lime-green values are only estimates is that the "outlier" selection (ignoring certain states from the reference value calculation) besides depending on a quantitative assessment also depends on a more complicated overall qualitative assessment, and hence it can not be predicted with absolute certainty which of the states the Commission will deem to be outliers. So any selection of outliers by the lime-green data lines shall only be regarded as qualified estimates, which potentially could be different from those outliers which the Commission would have selected if they had published a specific report at the concerned point of time.[nb 1] The national fiscal accounts for the previous full calendar year are released each year in April (next time 23 April 2015).[37] As the compliance check for both the debt and deficit criteria always awaits this release in a new calendar year, the first possible month to request a compliance check will be April, which would result in a data check for the HICP and interest rates during the reference year from 1 April to 31 March. Any EU member state may also ask the European Commission to conduct a compliance check, at any point of time during the remainder of the year, with HICP and interest rates always checked for the past 12 months – while debt and deficit compliance always will be checked for the three-year period encompassing the last completed full calendar year and the two subsequent forecast years.[38][39] As of 10 August 2015, none of the remaining euro derogation states without an opt-out had entered ERM-II,[40] which makes it highly unlikely that any of them will request that the European Commission conduct an extraordinary compliance check ahead of the publication of the next regular convergence report scheduled June 2016. Historical eurozone enlargements and exchange-rate regimes for EU membersFurther information: History of the euro

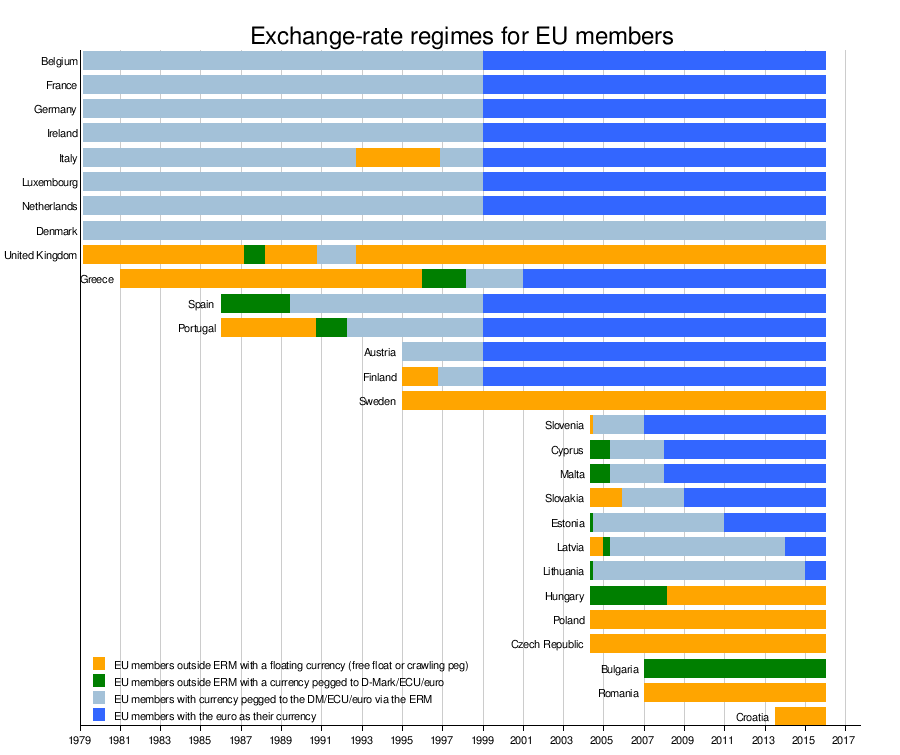

The chart below provides a full summary of all applying exchange-rate regimes for EU members, since the European Monetary System with its Exchange Rate Mechanism and the related new common currency ECU was born on 13 March 1979. The euro replaced the ECU 1:1 at the exchange rate markets, on 1 January 1999. During 1979–1999, the German mark functioned as a de facto anchor for the ECU, meaning there was only a minor difference between pegging a currency against ECU and pegging it against the German mark.  Sources: EC convergence reports 1996-2014, Italian lira, Spanish peseta, Portuguese escudo, Finish markka, Greek drachma, UK pound The eurozone was born with its first 11 Member States on 1 January 1999. The first enlargement of the eurozone, to Greece, took place on 1 January 2001, one year before the euro had physically entered into circulation. The next enlargements were to states which joined the EU in 2004, and then joined the eurozone on 1 January in the mentioned year: Slovenia (2007), Cyprus (2008), Malta (2008), Slovakia (2009),[1] Estonia (2011),[2] Latvia (2014),[3] and Lithuania (2015).[41] States obliged to join Eurozone participation

Apart from Denmark and the United Kingdom, which acquired opt-outs under the Maastricht Treaty, all other EU members are legally obliged to join the eurozone. The following members must first join ERM II before they can adopt the euro: BulgariaMain article: Bulgaria and the euro

The lev is not part of ERM-II, but since the launch of the euro in 1999, it has been pegged to the euro at a fixed rate of €1 = BGN 1.95583 through a strictly managed currency board.[nb 2] In all of the three latest annual assessment reports, Bulgaria managed to comply with four out of the five economic convergence criteria for euro adoption, only failing to comply with the criteria requiring the currency of the state to have been a stable ERM-II member for a minimum of two years.[42][43][44] Bulgarian Finance Minister Simeon Dyankov, originally planned to join ERM-II in 2009–10.[45][46][47] However, in July 2011 he explained that the government had decided not to adopt the euro, for as long as the European sovereign-debt crisis was still ongoing and unsolved, but that euro adoption could take place as early as 1 January 2015.[48] According to Deutsche Bank, the government had selected a target date for ERM-II entry of the beginning of 2013.[49] However, Bulgaria abstained from entering ERM-II during 2013 and 2014,[50] and stated that it had no intention to adopt the euro for as long as the eurozone debt crisis remained unsolved because they wanted certainty and clarity of all the consequences of adopting the euro before deciding to join.[51] In January 2015, the new elect Finance Minister Vladislav Goranov said, that it was absolutely possible for Bulgaria to join ERM-II before the term of the current government ends in 2018, and that he would begin talks with the Eurogroup to map what sort of preparations the state should undertake to qualify for membership.[52] The former governor of the Bulgarian National Bank, Kolyo Paramov, in office when the currency board of the state was established, believes the euro should be adopted in January 2018, because this would "trigger a number of positive economic effects": Sufficient money supply (leading to increased lending which is needed to improve economic growth), getting rid of the currency board which prevents the national bank functioning as a lender of last resort to rescue banks in financial troubles, and finally private and public lending would benefit from lower interest rates (at least half as high).[53] The former deputy governor of the Bulgarian National Bank, Emil Harsev, agreed with Paramov, stating that it was possible to adopt the euro already in 2018, and "Bulgaria’s membership in the eurozone will bring only positive effect on the economy" because "since establishing the currency board in 1997, we have been accepting all the negative effects of accession into the eurozone without getting the positive ones (access to the European financial market)".[54] In July 2015 Bulgaria approved the establishment of a co-ordination council to prepare the country for euro zone membership. The government has stated that among the main functions of the council will be drafting a national plan for the introduction of the euro in Bulgaria, a proposal to the Cabinet to determine the target date for euro adoption, organisation and coordination of the practical preparation of the country for euro membership and management and coordination of the work of the expert working groups.[55][56] According to a eurobarometer poll in April 2015, 55 percent of Bulgarians are in favour of introducing the euro (an increase of 4 percent from 2014), whereas 39 percent are opposed (a decrease of 6 percent from 2014).[57][58] CroatiaMain article: Croatia and the euro

Croatia's currency, the kuna, has used the euro (and prior to that one of the euro's major predecessors, the Deutsche Mark) as its main reference since its creation in 1994, and a long-held policy of the Croatian National Bank has been to keep the kuna's exchange rate with the euro within a relatively stable range. Prior to Croatia becoming a member of the EU on 1 July 2013, Boris Vujčić, governor of the Croatian National Bank, stated that he would like the kuna to be replaced by the euro as soon as possible after accession.[59] In its first assessment under the convergence criteria in May 2014, the country satisfied the inflation and interest rate criteria, but did not satisfy the public finances and ERM membership criteria.[60] The European Central Bank expects Croatia to be approved for ERM-II membership at the earliest in 2016, leading to a subsequent euro adoption at the earliest in 2019.[61] According to a eurobarometer poll in April 2015, 53 percent of Croatians are in favor of introducing the euro (a decrease of 2 percent from 2014), whereas 40 percent are opposed (an increase of 1 percent from 2014).[57][58] In April 2015, President Kolinda Grabar-Kitarovic stated in a Bloomberg interview she was "confident that Croatia would introduce the euro by 2020", while Prime Minister Zoran Milanovic said at the government session that "some occasional announcements when Croatia will introduce the euro shouldn't be taken seriously. We'll try to make it as soon as possible, but I distance myself from any dates and ask that you don't comment on it. When the country is ready, it will enter the euro area. The criteria are very clear."[62] Czech RepublicMain article: Czech Republic and the euro

Following their accession to the EU in May 2004, the Czech Republic aimed to replace the koruna with the euro in 2010, however this was postponed indefinitely.[63] The European sovereign-debt crisis further decreased the Czech Republic's interest in joining the eurozone.[64] Then Czech Prime Minister Petr Nečas said that because the conditions governing the eurozone had significantly changed since their accession treaty was ratified, he believed that Czechs should be able to decide by a referendum whether to join the Eurozone under the new terms.[65] In late 2010 a discussion arose within the Czech government, partially initiated by then President Václav Klaus, a well known eurosceptic, over negotiating an opt-out from joining the eurozone. Nečas later stated that an opt-out was unnecessary because the Czech Republic could not be forced to join the ERM II and thus could decide if or when to fulfil one of the necessary criteria to join the eurozone, an approach similar to the one taken by Sweden.[66][67] Miloš Zeman, who was elected President of the Czech Republic in early 2013, supports euro adoption by the Czech Republic, though he also advocates for a referendum on the decision.[68] Prior to being elected Prime Minister, Bohuslav Sobotka stated on 25 April 2013 that he was "convinced that the government that will be formed after next year's election should set the euro entry date" and that "1 January 2020 could be a date to look at".[69] In line with this, the governor of the Czech National Bank, having an advisory role towards the government about the timing of euro adoption, said that 2019 is the earliest possible euro entry date.[70][71] In December 2013, the Czech government approved a recommendation from the Czech National Bank and Ministry of Finance, against setting a formal target date for euro adoption or joining ERM-II in 2014.[72] In April 2014, the Czech Ministry of Finance confirmed in its Convergence Programme delivered to the European Commission that the country had not yet set a target date for euro adoption and would not apply for ERM-II membership in 2014. Their goal was to limit their time as an ERM-II member, prior to acceding to the eurozone, to as brief as possible. Moreover, it was the opinion of the previous government that: "the fiscal problems of the eurozone, together with continued difficulty to predict the development of the monetary union, do not create a favorable environment for the future adoption of the euro."[73] According to a Eurobarometer poll in April 2015, 29 percent of Czechs were in favour of introducing the euro (an increase of 13 percent from 2014), whereas 70 percent were opposed (a decrease of 7 percent from 2014)[57][58] Czech president Milos Zeman stated in June 2014, that he hoped his country would adopt the euro as soon as 2017, arguing that adoption would be beneficial for the Czech economy overall.[74] The opposition ODS party responded by running a campaign for Czechs to sign an anti-euro petition, handed over to the Czech Senate in November 2014, but viewed by political commentators as not having any changing impact of the government's policy to adopt the euro in the medium term without holding referendums about it.[75] In December 2014, the Czech government approved a joint recommendation from the Czech National Bank and Ministry of Finance, against setting a formal target date for euro adoption or joining ERM-II during the course of 2015.[76] In March 2015, the ruling Czech Social Democratic Party decided at its annual congress to adopt the policy of striving hard to gather political support for the state to adopt the euro by 2020, as one of their four top priorities.[77] In April 2015, the coalition government announced it had agreed not to set a euro adoption target and not to enter ERM-2 before after the next legislative election scheduled for 2017, making it unlikely that the Czech Republic will adopt the euro before 2020. In addition, the coalition government agreed that if it wins re-election it would set a deadline of 2020 to agree on a specific euro adoption roadmap.[78] HungaryMain article: Hungary and the euro

With their accession to the EU in 2004, Hungary began planning to adopt the euro in place of the forint. However, the country's high deficit delayed this. After the 2006 election, Prime Minister Ferenc Gyurcsány introduced austerity measures, reducing the deficit to less than 5% in 2007 from 9.2%. In February 2011, newly elected Prime Minister Viktor Orbán, of the soft eurosceptic Fidesz party, made clear, that he did not expect the euro to be adopted in Hungary before 1 January 2020.[79] Orbán said the country was not yet ready to adopt the currency and they will not discuss the possibility until the public debt reaches a 50% threshold.[80] The public debt-to-GDP ratio was 81.0% when Orban's 50% target was set in 2011, and it is currently forecast to decline to 73.5% in 2016.[81] In April 2013, Viktor Orbán proclaimed euro adoption would not happen until the Hungarian purchasing power parity weighted GDP per capita had reached 90% of the eurozone average.[82] According to Eurostat, this relative percentage rose from 57.0% in 2004 to 63.4% in 2014.[83] If the same pace of "catching up" progress was to be expected in the future as in the past ten years (6.4% per decade), Hungary would only reach Orban's 90% target and adopt the euro in 2056. Although, Hungary could potentially also reach Orban's 90% target and adopt the euro in 2033, if being able for the upcoming period to sustain the same 1.4% of annual improvements in the figure as achieved from 2013 to 2014. Shortly after Viktor Orbán had been re-elected as Prime Minister for another four-year term in April 2014,[84] the Hungarian Central Bank announced they plan to distribute a new series of Forint bank notes in 2018.[85] In June 2015, Orbán himself declared that his government would no longer entertain the idea of replacing the forint with the euro in 2020, as was previously suggested, and instead expected the forint to remain “stable and strong for the next several decades”,[86] although, On July 2016, National Economy Minister Mihály Varga suggested that country could adopt the euro by the “end of the decade”, but only if economic trends continue to improve and the common currency becomes more stable.[87][88] No official target date has been set for euro adoption. According to a eurobarometer poll in April 2015, 60 percent of Hungarians are in favor of introducing the euro (a decrease of 4 percent from 2014), whereas 35 percent are opposed (an increase of 5 percent from 2014).[57][58] PolandMain article: Poland and the euro

Article 227 of the Constitution of the Republic of Poland[89] will need to be amended to allow a change of the Polish currency from the złoty to the euro. In December 2011 Polish foreign minister Radosław Sikorski said that Poland aimed to adopt the euro on 1 January 2016, but only if "the eurozone is reformed by then, and the entrance is beneficial to us."[90] In the autumn of 2012 the Monetary Policy Council of the Polish National Bank published its official monetary guidelines for 2013, confirming earlier political statements that Poland should only join the ERM II once the existing eurozone countries had overcome the ongoing sovereign-debt crisis, to "maximise the benefits of monetary integration and minimise associated costs".[91] In late 2012, Polish Prime Minister Donald Tusk announced that he planned to launch a "national debate" on euro adoption the following spring, and in December 2012 Polish Finance Minister Jacek Rostowski said that his country should strive to adopt the euro as soon as possible. However, the opposition Law and Justice Party opposes euro adoption and the governing parties do not have enough seats in the Sejm to make the required constitutional amendment.[92][93] In January 2013, Polish President Bronislaw Komorowski stated that a decision on euro adoption should not be made until after parliamentary and presidential elections scheduled for 2015, but that in the meantime the country should try to comply with the convergence criteria.[92] In February 2013, Jaroslaw Kaczynski, leader of the Law and Justice Party stated that "I do not foresee any moment when the adoption of the euro would be advantageous for us" and called for a referendum on euro adoption.[94] In March 2013, Tusk said for the first time that he would be open to considering a referendum on euro participation, decided by a simple majority, provided that it was part of a package in which the parliament first approved the necessary constitutional amendment to adopt the euro subject to approval in a referendum.[95] In April 2013 Marek Belka, head of National Bank of Poland, said that Poland should demand to be permitted to adopt the euro without first joining the ERM-II, due to concerns over currency speculation.[96] In June 2014, a joint statement by the finance minister, central bank chief and president of Poland stated that Poland should begin a debate shortly after the 2015 parliamentary election about when to adopt the euro,[97] leading to a roadmap decision that might even include identification of a target date.[98] In October 2014, the Deputy Prime Minister Janusz Piechociński suggested that Poland should join the Eurozone in 2020 at the earliest.[99] The new elect Prime Minister, Ewa Kopacz, having replaced Donald Tusk for the remaining last year of the governments term, at the same time commented: "Before answering the question which target date should be set for the euro changeover, we must ask another: What is the situation of the eurozone and where are they going? If the eurozone will strengthen, then Poland should fulfill all the criteria for inclusion, which would in any case be good for the economy."[100] The PM hereby referred to the earlier political decision of first letting the National Coordination Committee for Euro Changeover complete its update of the changeover plan, which await a prior establishment of the banking union, before setting a target date for euro adoption.[nb 3] Polls have generally showed that Poles are opposed to adopting the euro straight away,[64][103] with a eurobarometer poll in April 2015 showing that 44 percent of Polish people are in favour of introducing the euro (a decrease of 1 percent from 2014), whereas 53 percent are opposed (no change from 2014).[57][58] However, polls conducted by TNS Polska throughout 2012–2015 have consistently shown support for eventually adopting the euro,[104][105][106][107][108][109][110][111][112] though that support depends on the target date. According to the latest TNS Polska poll from June 2015, the share who supported adoption was 46% against 41%. When asked about the appropriate timing, the supporters were divided into three groups of equal size, with 15% advocating for adoption within the next 5 years, another 14% preferring it should happen between 6–10 years from now, and finally 17% arguing it should happen more than 10 years from now.[112] RomaniaMain article: Romania and the euro

Originally, the euro was scheduled to be adopted by Romania in place of the leu by 2014.[113] In April 2012 the Romanian convergence report submitted under the Stability and Growth Pact listed 1 January 2015 to be the target date for euro adoption.[114] The governor of the National Bank of Romania argued in November 2012 that it had been a financial benefit for Romania to not be a part of the euro area during the European debt crisis, but that the country in the years ahead would strive to comply with all the convergence criteria.[115] In April 2013 Romania submitted their annual Convergence Programme to the European Commission, which for the first time did not specify a target date for euro adoption.[116][117] Prime Minister Victor Ponta has stated that "eurozone entry remains a fundamental objective for Romania but we can't enter poorly prepared", and that 2020 was a more realistic target.[117] The following year, Romania's Convergence Report set a target date of 1 January 2019 for euro adoption.[118][119] According to the Erste Group Bank, it would be very difficult for Romania to meet this 2019 target, not in regards of complying with the five nominal convergence criteria values, but in regards of reaching some appropriate levels of real convergence (i.e. raising the GDP per capita from 50% to a level above 60% of the EU average) ahead of the euro adoption.[120] The Romanian Central Bank governor, Mugur Isărescu, admitted the target was ambitious, but obtainable if the political parties passed a legal roadmap for the required reforms to be implemented, and clarified this roadmap should lead to Romania entering ERM-2 only on 1 Jan 2017 so the euro could be adopted after two years of ERM-2 membership on 1 Jan 2019.[121] In April 2015, Isărescu stated that the technical requirement for adoption of the euro 1 January 2019 would imply joining ERM-2 at the latest in the first half of 2016. Ahead of ERM-2 entry, Isărescu argued, Romania needs to conduct monetary adjustments in form of finalizing the process of bringing minimum reserve requirement ratios in line with eurozone levels (a process envisaged to last between 1-1½ year) and to complete major economic policy adjustments: 1) Removing the sources of repressed inflation (i.e. completion of the energy market deregulation), 2) Removing sources of quasi-fiscal deficits (by restructuring loss-making state-owned enterprises), 3) Removing other sources of future budgetary pressures (i.e. the unavoidable expenditures to modernise road infrastructure).[122] As of April 2015, the Romanian government concluded it was still on track to attain its target for euro adoption in 2019, both in regards of ensuring full compliance with all nominal convergence criteria and in regards of ensuring a prior satisfying degree of "real convergence". The Romanian target for "real convergence" ahead of euro adoption, is for its GDP per capita (in purchasing power standards) to be above 60% of the same average figure for the entire European Union, and according to the latest outlook, this relative figure was now forecast to reach 65% in 2018 and 71% in 2020,[123] after having risen at the same pace from 29% in 2002 to 54% in 2014.[83] Finally, the Romanian government also expressed its commitment fully to join all pillars of the Banking Union, as soon as possible.[123] According to a eurobarometer poll in April 2015, 68 percent are in favor of introducing the euro (a decrease of 6 percent from 2014), whereas 26 percent are opposed (an increase of 2 percent from 2014).[57][58] SwedenMain article: Sweden and the euro

Although Sweden is required to replace the krona with the euro eventually, it maintains that joining the ERM II, a requirement for euro adoption, is voluntary,[124][125] and has chosen to not join pending public approval by a referendum, thereby intentionally avoiding the fulfillment of the adoption requirements. On 14 September 2003 56% of Swedes voted against adopting the euro in a referendum.[126] Most of Sweden's major parties believe that it would be in the national interest to join, but they have all pledged to abide by the result of the referendum. Former Prime Minister Fredrik Reinfeldt stated in December 2007 that there will be no referendum until there is stable support in the polls.[127] The polls have generally showed stable support for the "no" alternative, except some polls in 2009 showing a support for "yes". Since 2010 the polls showed strong support for "no" again. According to a eurobarometer poll in April 2015, 32 percent of Swedes are in favor of introducing the euro (an increase of 9 percent from November 2014), whereas 66 percent are opposed (a decrease of 7 percent from November 2014).[58][128] States not obliged to joinDenmarkMain article: Denmark and the euro

Denmark has pegged its krone to the euro at €1 = DKK 7.46038 ± 2.25% through the ERM II since it replaced the original ERM on 1 January 1999. During negotiations of the Maastricht Treaty of 1992, Denmark secured a protocol which gave it the right to decide if and when they would join the euro. Denmark subsequently notified the Council of the European Communities of their decision to opt out of the euro. This was done in response to the Maastricht treaty having been rejected by the Danish people in a referendum earlier that year. As a result of the changes, the treaty was ratified in a subsequent referendum held in 1993. On 28 September 2000, a euro referendum was held in Denmark resulting in a 53.2% vote against the government's proposal to abrogate the euro opt-out. Since 2007, the Danish government has discussed holding another referendum on euro adoption.[129] However, the uncertainty, both in terms of the stability of the euro and the establishment of new political structures at the EU level, resulting first from eruption of the Financial Crisis and then subsequently from the related European government-debt crisis, led the government to postpone the referendum to a date after the end of its legislative term. When a new government came to power in September 2011, they outlined in their government manifest, that a euro referendum would not be held during its four-year term, due to a continued prevalence of this uncertainty.[130] As part of the European elections in 2014, it was argued collectively by the group of pro-European Danish parties (Venstre, Konservative, Social Democrats and Radikale Venstre), that an upcoming euro referendum would not be in sight until the "development dust had settled" from creation of multiple European debt crisis response initiatives (including the establishment of Banking Union, and the Commission's - still in pipeline - proposal package for creating a strengthened genuine EMU). When a new Venstre-led government came to power in June 2015, their government manifest did not include plans for holding a euro referendum within their four-year legislative term.[131] Opinion polls, which had generally favoured euro adoption from 2002 to 2010, showed a rapid decline in support during the height of the EU debt crisis,[132] reaching a low in May 2012 with 26% in favor towards 67% against while 7% were in doubt.[133] United KingdomMain article: United Kingdom and the euro

The United Kingdom entered the ERM in October 1990. The UK government spent over £6 billion trying to keep its currency within the narrow limits prescribed by ERM, but was forced to exit the programme within two years after its currency the pound sterling came under major pressure from currency speculators. The ensuing crash of 16 September 1992 was subsequently dubbed "Black Wednesday". During the negotiations of the Maastricht Treaty of 1992 the UK secured an opt-out from adopting the euro.[134] The Labour government of Tony Blair argued that the UK should join the euro, contingent on approval in a referendum, if five economic tests were met. The UK Treasury first assessed tests in October 1997, when it was decided that the UK economy was neither sufficiently converged with that of the rest of the EU, nor sufficiently flexible, to justify a recommendation of membership at that time. The assessment of June 2003 concluded that not all were met.[135] The Conservative-Liberal Democrat coalition government elected in 2010 pledged not to join the euro during its term of office,[136][137] due to expire in 2015. The Conservative government that followed the coalition does not have any plans for euro adoption; rather, it held a referendum on continuing to be a member of the EU at all, which resulted in a vote in favour of leaving the EU by 52%.[4][5][6][7] Outside the EUSee also: Future enlargement of the European Union

The EU's position is that no independent sovereign state is allowed to join the eurozone without first being a full member of the European Union (EU). However, four independent sovereign European microstates situated within the borders of the eurozone states, have such a small size — rendering them unlikely ever to join the EU — that they have been allowed to adopt the euro through the signing of monetary agreements, which granted them rights to mint local euro coins without gaining a seat in the European Central Bank. In addition, some dependent territories of EU member states have also been allowed to use the euro without being part of the EU, conditional the signing of agreements where a eurozone state guarantee their prior adoption of regulations applying specifically for the eurozone. IcelandDuring the 2008–2011 Icelandic financial crisis, instability in the króna led to discussion in Iceland about adopting the euro. However, Jürgen Stark, a Member of the Executive Board of the European Central Bank, has stated that "Iceland would not be able to adopt the EU currency without first becoming a member of the EU".[138] Iceland subsequently applied for EU membership. As of the ECB's May 2012 convergence report, Iceland did not meet any of the convergence criteria.[139] One year later, the country had achieved compliance with the deficit criteria and had begun to decrease its debt-to-GDP ratio,[140] but still suffered from elevated HICP inflation and long-term governmental interest rates.[21][23] On 13 September 2013, a newly elected government dissolved the accession negotiation team and thus suspended Iceland's application to join the European Union until a referendum can be held on whether or not the accession negotiations should resume; if negotiations do resume, after they are completed the public will then have the opportunity in a second referendum to vote on "whether or not Iceland shall join the EU on the negotiated terms".[141][142][143] Kosovo and MontenegroFurther information: Kosovo and the euro and Montenegro and the euro

Kosovo[lower-alpha 1] and Montenegro have unilaterally adopted and used the euro since its launch, as they previously used the German mark rather than the Yugoslav dinar. This was due to political concerns that Serbia would use the currency to destabilise these provinces (Montenegro was then in a union with Serbia) so they received Western help in adopting and using the mark (though there was no restriction on the use of the dinar or any other currency). They switched to the euro when the mark was replaced, but have signed no monetary agreement with the ECB; rather the country depends only on euros already in circulation.[149][150] Kosovo also still uses the Serbian dinar, which replaced the Yugoslav dinar, in areas mainly populated by the Serbian minority.[151] European microstates

The European microstates of Monaco, San Marino and the Vatican City, which had a monetary agreement with a eurozone state when the euro was introduced, were granted a special permission to continue these agreements and to issue separate euro coins, but they don't get any input or observer status in the economic affairs of the eurozone. Andorra, which had used the euro unilaterally since the inception of the currency, negotiated a similar agreement which granted them the right to officially use the euro as of 1 April 2012 and to issue euro coins.[19] Liechtenstein, situated on the border of Switzerland, opted instead to sign a monetary agreement making the Swiss franc their legal tender since 1920, and so far has not expressed any interest in adopting the euro. Dependent territories of EU member states — outside EUFour of the dependent territories of EU member states not part of the EU, have nevertheless adopted the euro:

Faroe Islands and GreenlandThe Danish krone is currently used by both of its dependent territories, Greenland and Faroe Islands, with their monetary policy controlled by the Danish Central Bank.[163] If Denmark does adopt the euro, separate referendums would be required in both territories to decide whether they should follow suit. Both territories have voted not to be a part of the EU in the past, and their populations will not participate in the Danish euro referendum.[164] The Faroe Islands use a special version of the Danish krone notes that have been printed with text in the Faroese language.[165] It is regarded as a foreign currency, but can be exchanged 1:1 with the Danish version.[163][165] On 5 November 2009 the Faroese Parliament approved a proposal to investigate the possibility for euro adoption, including an evaluation of the legal and economic impact of adopting the euro ahead of Denmark.[166][167][168][169] New Caledonia, French Polynesia and Wallis and FutunaThe CFP franc is currently used as a euro pegged currency by three French overseas collectivities: French Polynesia, Wallis and Futuna and New Caledonia. The French government has recommended that all three territories decide in favour of adopting the euro. French Polynesia has declared themselves in favour of joining the eurozone. Wallis and Futuna announced a neutral standpoint, that they would support a currency choice similar to what New Caledonia chooses. However, New Caledonia has not yet made any decision, because they first await the fallout of an independence referendum, scheduled to be held at the latest in November 2018,[lower-alpha 2] as this might influence their opinion whether or not to adopt the euro. If the three collectivities decide to adopt the euro, the French government would make an application on their behalf to the European Council, and the switch to the euro could be made after a couple of years. If the collectivities fail to reach a unanimous decision about the future of the CFP franc, it would be technically possible to implement an individual currency decision for each territory.[171] Summary of adoption progress

See also: History of the euro

Article 140 of the Treaty on the Functioning of the European Union requires the European Commission and the ECB to report to the Ecofin Council at least once every two years, or at the request of a Member State with a "euro derogation", on the progress made by states to comply with the euro adoption criteria and their suitability to join the eurozone. The most recent report was published 4 June 2014, and covered the then 8 remaining non-euro member states without an opt-out: Lithuania, Poland, Czech Republic, Hungary, Romania, Bulgaria, Croatia and Sweden.[173] Lithuania's adoption of the euro on 1 January 2015 was given final approval by the Council of the European Union on 23 July 2014.[41] As reported by the table below, the remaining seven new EU members are expected to take longer to adopt the euro. This is in part due to the challenges caused by the 2008 financial crisis, as well as the necessity for their economies to catch up to European standards after recently joining the EU's internal market, before being able to comply with all the economic convergence criteria.[174] Each country aspiring to adopt the euro has been requested by the European Commission to develop a "strategy for criteria compliance" and "national euro changeover plan". In the "changeover plan", the country can select from between three scenarios for euro adoption:[175]

The second scenario is recommended for candidate countries, while the third is only advised if at a late stage in the preparational process they experience technical difficulties (i.e. with IT systems), which would make an extended transitional period for the phasing out of the old currency at the legal level a necessity.[175] The European Commission has published a handbook detailing how states should prepare for the changeover. It recommends that a national steering committee is established at a very early stage of the state's preparation process, with the task to outline detailed plans for the following five actions:[176]

The table below summarizes each candidate country's national plan for euro adoption and currency changeover.[178]

The 2008 financial crisis caused a delay in the schedule for adoption of the euro for most of the new EU members. The convergence progress for the newly accessed EU member states, is supported and evaluated by the yearly submission of the "Convergence programme" under the Stability and Growth Pact. As a general rule, the majority of economic experts recommend for newly accessed EU member states with a forecasted era of catching up and a past record of "macroeconomic imbalance" or "financial instability", that these countries first use some years to address these issues and ensure "stable convergence", before taking the next step to join the ERM-II, and as the final step (when complying with all convergence criteria) ultimately adopt the euro. In practical terms, any non-euro EU member state can become an ERM-II member whenever they want, as this mechanism does not define any criteria to comply with. Economists however consider it to be more desirable for "unstable countries", to maintain their flexibility of having a floating currency, rather than getting an inflexible and partly fixed currency as an ERM-II member. Only at the time of being considered fully "stable", the member states will be encouraged to enter into ERM-II, in which they need to stay for a minimum of two years without presence of "severe tensions" for their currency, while at the same time also ensuring compliance with the other four convergence criteria, before finally being approved to adopt the euro.[174] The table below has mapped the historic exchange rate developments for the remaining states with a euro derogation, pre and post of the 2008 financial crisis. Positive percentage changes are equal to a depreciation of the local currency, while negative percentage changes are equal to an appreciation of the local currency. For all of the remaining non-eurozone states in Central and Eastern Europe with a free-floating currency (Czech Republic, Hungary, Poland, Romania), having economies characterized by being engaged in an ongoing significant catching up process — moving closer year by year towards the average values of the eurozone, the aftermath of the financial crisis resulted in severe currency devaluations (see the figures displayed by the 2014/2008 column in the table below).

The exchange rate developments for the non-eurozone states outside ERM-2, comprised more moderate appreciations/depreciations for the latest year (see the figures displayed by the 2015/2014 column in the table above). See alsoNotes and referencesNotes

References

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||